Starting your first job is one of life’s most exciting times. While you are enjoying the freedom of financial independence, it is crucial to develop good money management skills to keep you on a solid financial footing.

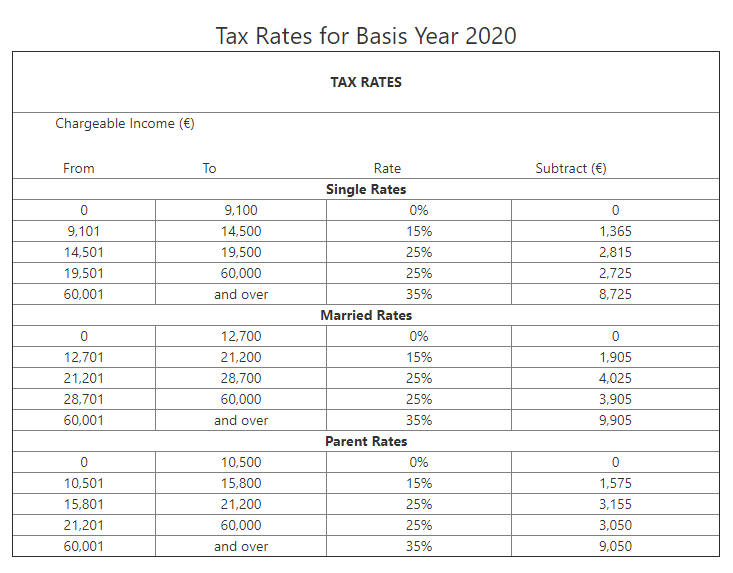

The Table below presents the tax rates for basis year 2020.

https://cfr.gov.mt/en/rates/Pages/TaxRates/Tax-Rates-2020.aspx

Go to our Calculators section or click here to download for free the tax calculator that matches your civil status.

Go to our Calculators section or click here to download for free the tax calculator that matches your civil status.

Depending on your income and whether single rates, married rats or parent rates apply, depending on your case, your employer will deduct from your wage or salary the income tax owed and your social security contribution. This means you will receive a wage or salary that is net of income tax and social security contributions.

In the second quarter of a new year your employer will provide you with a form titled ‘FS3’. This form will show the total income you received during the previous year – including fringe benefits, allowances, etc. – and the income tax and social security contributions you paid during the course of the year. In case of more than one employment, you will receive such an ‘FS3’ form from each employer.

You are to submit your income tax form, each year, by not later than 30th June. It is important that you submit this form on time as you will otherwise incur penalties for late filing of tax return forms. Any tax arrears can be paid on-line. Click here for more information.

It is important to check your payslip to see you are getting the right pay. Employers do make mistakes.

If you are paid by the hour, it is best to jot down the punch in and punch out time on a notebook or you may download free timesheet apps to keep track of the hours worked.

While you may be thrilled by the purchase power of your wage because of your first job, make sure that your spending does not exceed your income. You might wish to read our below posts.

Buying a house, getting married, having a first child, retiring – may all seem a long way off. Most probably your immediately priority would be to buy a car. Before you do so make it a habit to save part of your income every month. Regular saving is an excellent habit to get into and the earlier you start saving, the more money you will have to meet your various financial goals during the rest of your working life and in retirement.

You may wish to consider taking out a private retirement pension plan – now available on the market – so that you start preparing for your retirement – far away as it may seem to be. It is never too early nor too late to start planning for your retirement. Think of the day you headed off to kindergarten with your parents’ hoping to prepare you for success in a world that seemed years away – suddenly you are there. Likewise, you need to prepare for your retirement well in advance. Thanks to various financial products like the power of compound interest, the earlier you start saving the faster your savings will grow.

Budgeting involves making a list of all your expenses, and comparing it against your cash inflows. Use Gemma’s budget calculator to record all of your incomings and outgoings, which gives a breakdown of where your spending goes each week, month, year and what your cash inflows are. Once you have a clear idea of your budget, work out a fixed amount that you can save each month and stick to it.